Unfunded Obligations

Massive Debt & Growing

We're Living Longer

The G-Fund

U.S. National Debt

The current U.S. national debt:

$34,581,882,240,753

Much of your portfolio is most likely at risk...click on the button below to learn how much and what you can do about it to ensure peace of mind.

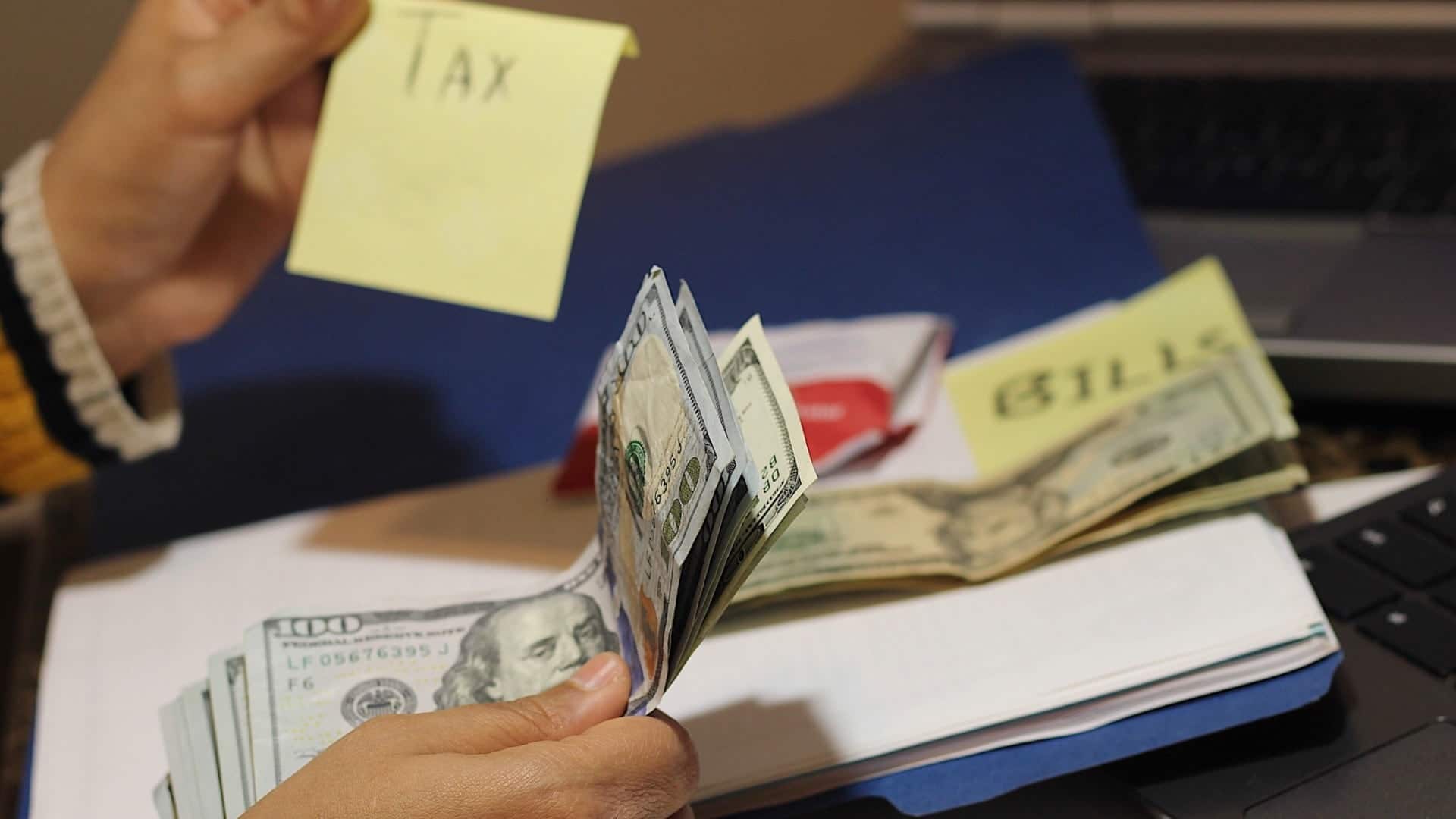

https://vimeo.com/469501921 In this vlog/blog, I’m going to be addressing the issue of tax increases in the future. And nobody actually knows what taxes are going

https://vimeo.com/470033007 Today I’m talking about taxes and retirement, specifically taxation in retirement. Not a huge, obvious topic for most folks, which is why it gets

Unfunded Obligations Massive Debt & Growing We’re Living Longer The G-Fund Social Media